When cryptocurrencies were first introduced with Bitcoin it was meant to be a peer-to-peer global payment system but it failed. Bitcoin is abnormally volatile for use in regular transactions. A bitcoin can fluctuate from $100,000 to $80,000 in a day and go back. This makes it use in a real world transaction impractical and this also warrants bitcoin being classified as an investment and not a currency. While the system failed, the thesis behind the system still held true. The global financial system is riddled with inefficiencies that affect small businesses and consumers alike - cryptocurrency seems to be the answer, we just didn’t know in what form.

Stablecoin a form of cryptocurrency that is pegged to a real world asset is an emerging answer. Unlike Bitcoin which derives its value from supply and demand dynamics and a perception of value (not too much unlike gold), there is a real driver of value for stablecoins in the form of real world assets. These could be gold, bonds, dollars, or any other such assets. Just for the sake of completeness, there have been other forms of stablecoins in the past, such as algorithmic stablecoins (automatic print and destruction of currency based on algos) but those are not real stablecoins; they are a more sophisticated form of Bitcoin itself. The Luna Terra scandal, where a lot of people lost a lot of money, was driven by these algorithmic stablecoin. A stablecoin, by definition, is one that is pegged to a real asset.

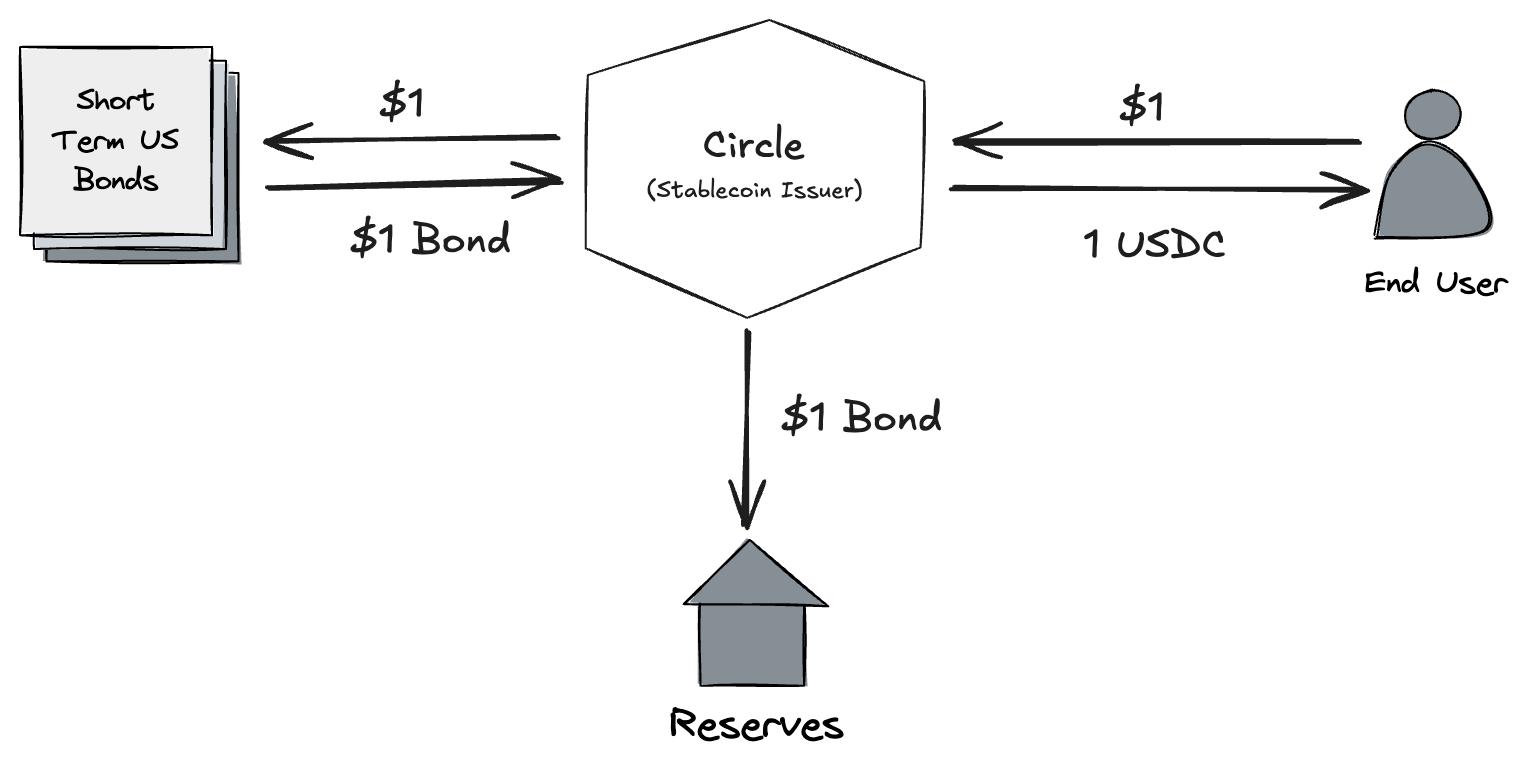

Let’s understand stablecoins more fundamentally through the example of the 2 most widely used (~90% market share) coins - USDT (issued by Tether) and USDC (issued by Circle). Imagine you purchase $1 worth of the stablecoin USDC from Circle. They will take your $1, issue you stable coin worth $1 and simultaneously buy short-term US Treasury Bills worth $1. Thus, your coin is 1:1 pegged to the US Treasury. When you redeem that USDC, Circle sells the Treasury bill (or equivalent reserve asset) and returns your dollar. Hypothetically, the peg could be 1:10 or 1:100 as well, but to build trust in the system, the 2 top players (Circle & Tether) are going with a 1:1 peg with the treasury bills. Stablecoins can be thought of as tokenized dollars (or gold, or bonds) that work on crypto rails. They carry the stability of traditional finance, but with the programmability, speed, and borderless reach of blockchains.

Is this just a new banking system?

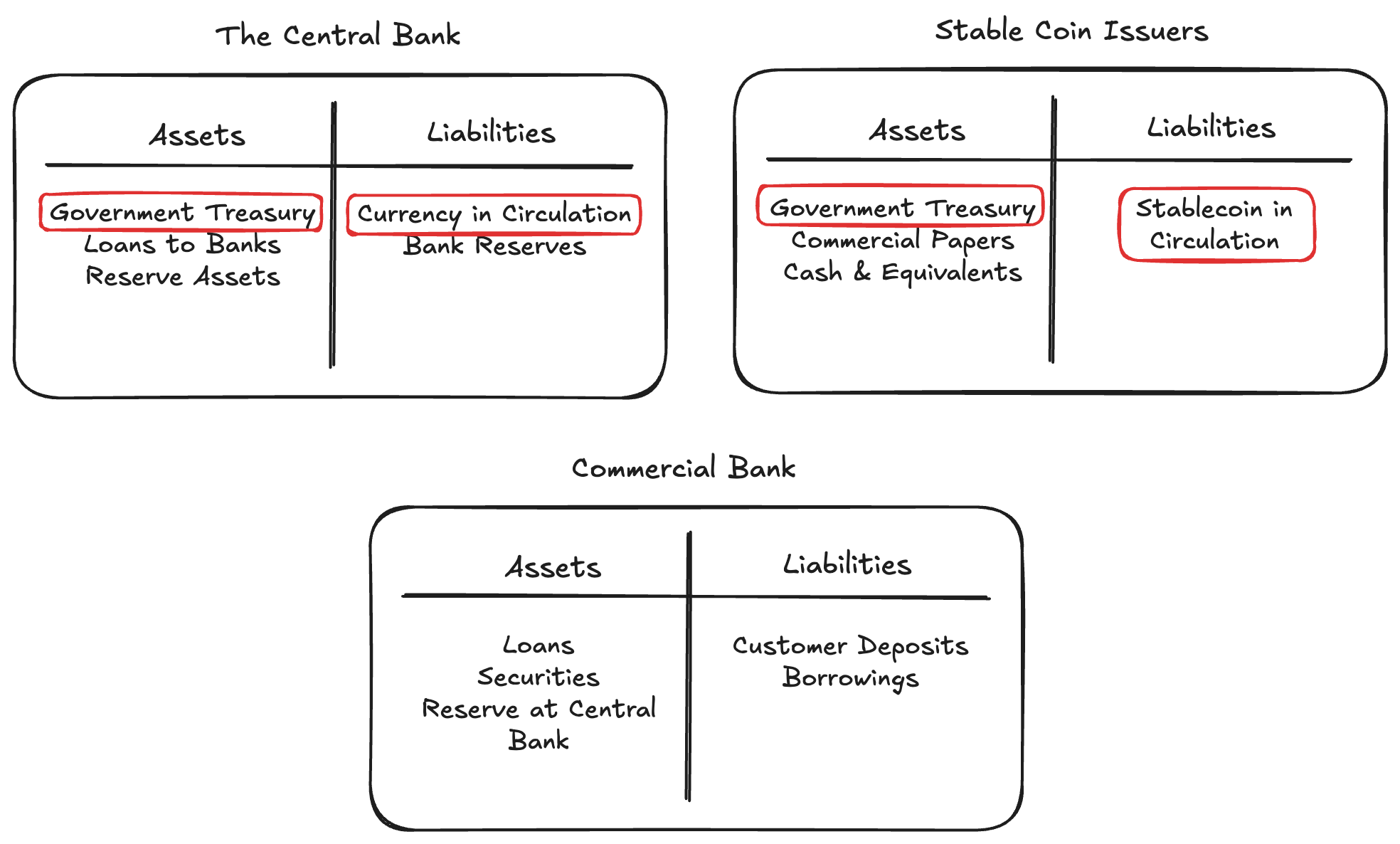

When we look at the Balance Sheet of companies like Tether or Circle, they have US treasuries on their Asset Side and Stablecoins issued on their Liabilities Side much like a Central Bank. Here’s a snapshot of the balance sheets of the Central Bank, a stablecoin issuer and a bank side-by-side:

If you look at the Balance Sheet of a Central Bank such as RBI and that of a Stablecoin issuer such as Tether, you see that they are almost similar. Both are creating currency and are backing it with government debt. The central bank issues sovereign money while Stable coin issuers issue private currency. Stablecoin issuers primarily earn through the interest earned on these government securities. This is much lower than in the case of banks, who create money in the economy through keeping only a part of the money deposited and lending the rest in the form of loans.

A fun fact before we move ahead, stablecoins issuers as of June 2025 (before the GENIUS Act was passed) held about $182 Billion worth US T-Bills putting them at the 17th largest US Debt holder, right after Mutual Funds, Insurance Houses and a few countries.

Revisiting Why Stablecoins?

Now that we understand stable coins as a concept, let’s go back again to why they are important. Multiple interesting factors together make stable coin the potential future (or step in the direction) of the financial system. Here are the reasons:

Stablecoins aren’t a speculative asset. There is very little value by investing in a stable coin like USDC. The only upside is through yield on the T-Bills and why would you invest in stablecoins for that.

Stablecoins are inherently stable. Because of it’s peg to a real world asset, they derive their value from something that can be easily valued and thus wild swings observed in purely speculative assets such as Bitcoins are absent in this currency.

Stablecoins are seeing favorable regulatory environment. Governments around the world are recognizing stablecoins as a form of currency. In the US, the GENIUS Act and in the EU, the MiCA is a push towards creating regulation around using stablecoins as a currency. In countries like India, the government is exploring CBDC - Central Bank Digital Currency - which for all intents and purposes are essentially stable coins issued by the government.

These make it perfect contender to solve for two of the biggest issues the international monetary systems are facing - the velocity of money and the cost of transactions. Velocity of money is how fast money can be transferred from one account to the other while cost of transaction is the fee you must pay to do that transfer. Let’s look at the biggest use case of stablecoins as of 2025:

Domestic Payment Infrastructure: On a domestic level, the cost of money is much bigger issue for countries like the US given that India already has UPI that has greatly increased the velocity of money while keeping the cost of transaction near zero. But in the US, credit card (primary mode of payment) transaction fees goes up to 2.5% which hurts the smaller businesses and end consumers. According to a16z, this can be brought down to as low as 0.3% in the stablecoin world.

Cross-border Remittances: While UPI has made domestic payments a cake walk, on an international level, you might lose upto the 10% of your transfer amount as fees with time for transfers going up to weeks if not months for larger transactions. There are often cases where you do not even know how much money you’ll eventually end up getting.

Hedge against Hyperinflation: The base use case of velocity aside, stable coins are also seen as a store of value and stability in hyperinflation economies such as Argentina or Venezuela. In Argentina, some local tax authorities accept tax payments in Crypto while in Venezuela, stablecoins like USDT have effectively replaced the bolívar for many transactions including groceries, rents, and wages.

Programmable Money: Micropayments across the world, AI Agent’s wallet for paying on your behalf, auto-settling of transactions in smart contracts with all the guard rails are just some of the major use cases of programmable money. Stablecoins are a form of currency that you can literally code for your required use cases.

DeFi Engine: Without stablecoins, Decentralized Finance (DeFi) as we know it would be practically impossible. DeFi aims to recreate the entire financial system (lending, borrowing, exchanges, derivatives) on a blockchain, but this is unachievable using a volatile asset like Bitcoin or Ethereum as the base currency.

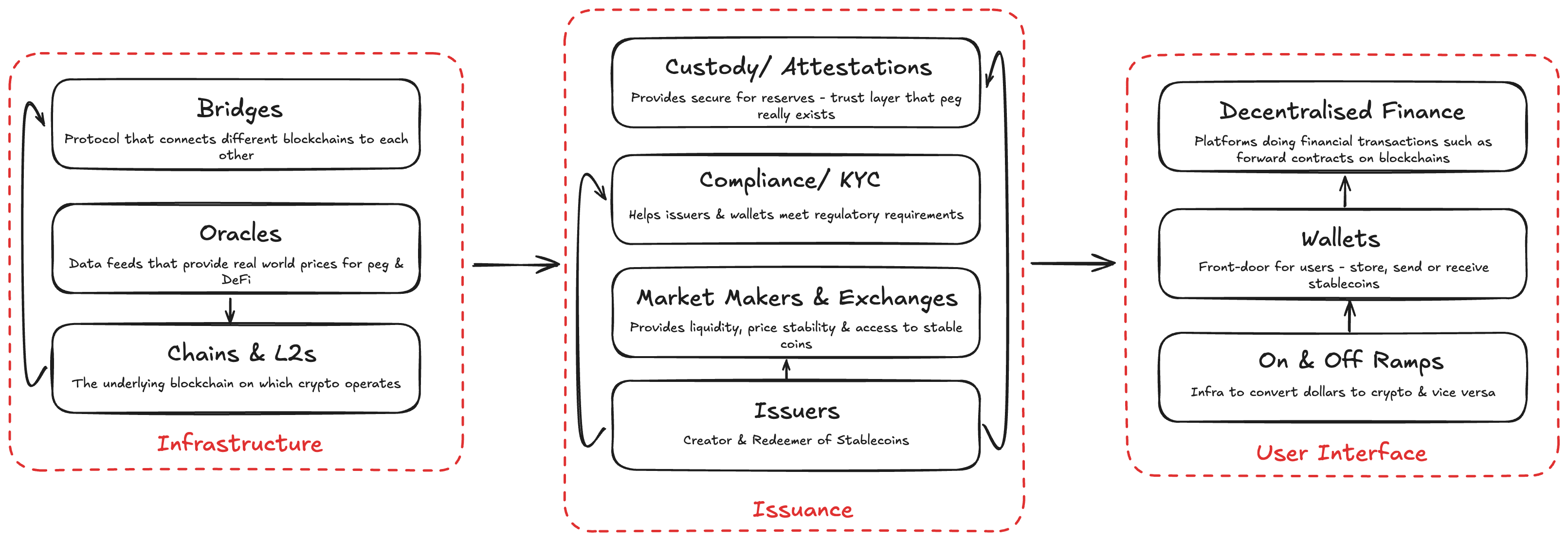

The Stablecoin Value Chain

Let’s understand in details what the value chain of stablecoins looks like and what kind of value is created where:

Infrastructure: The rails on which stablecoins operates

Chains & L2s:

Chains (or L1s) are the blockchains on which stablecoins are hosted. This is also where the actual transaction happens. Ethereum & Tron are 2 popular chains which have >85% of the market.

Layer 2s (L2s) are scaling solutions built on top of L1s to lower fees and increase the throughput of transactions enabling micropayments to become feasible. There is a rapid growth in transaction count and DeFi usage on L2s

Companies - Ethereum, Polygon & Tron in L1, Solana & Base in L2

Opportunity - Chains for Specific Industries (eg. SOL for micropayments or messaging apps)

Bridges:

These are protocols or platforms that connect multiple blockchains - eg. connecting Solana to Base. This is also the most vulnerable and hacked part of the value chain yet sees billions of dollars in daily transaction volumes.

This is critical for multi-chain apps, cross-chain composability & interoperability which is essential for setting up global payment routing.

Companies - Wormhole, LayerZero, Axelar

Oracles:

These are data feeds that deliver real world prices, foreign exchange rates, interest rates etc to the smart contracts. Oracles are crucial for protocol security ensuring price accuracy for pegs and DeFi ops. Billions in volume per day are channeled through oracles daily.

Companies - Chainlink (>70% Market Share), Pyth, Band Protocol

Opportunity - Niche Oracles such as Carbon Credits

Issuance: The issue & redemption of stablecoins

Stablecoin Issuers:

There are the firms that actually create stablecoins. These are typically regulated fintechs, crypto companies or even traditional finance companies. They guarantee the fiat peg and are the foundational trust layer for stablecoins. These firms typically earn through the interest rate earned from the reserve bonds, transaction fees or some partnerships.

The market (>$230B in market cap) is highly concentrated with the top 2 players having >90% market share.

Companies - Tether (USDT), Circle (USDC)

Opportunity - Regional coins or nice industry-specific coins for carbon credits

Custodians & Attestations:

Platforms that provide secure storage for reserves are custodians. They are supposed monthly attestations and need to attest to proof of reserves (this process is getting increasingly standardised). The key metric they are measured on is Assets under Custody (AUC). This is the trust layer that proves that the peg exists. The current market has tens of billions in AUC.

Their revenue model is straightforward. They earn primarily from some fees on their AUC and insurances

Companies - FireBlock, Coinbase Custody

Opportunity - Real-time Attestation system

Compliance & KYC:

This is the infrastructure for Anti-money Laundering (AML), KYC and other regulatory reporting. They help issuers and wallets meet their regulatory needs. The RegTech space is growing fast with new rules in the form of GENIUS and MiCA Act.

This can also be looked as the “cost of admission” for enterprise adoption. Given the cross-border complexity involved in stablecoins, there is a growing demand for tools for adapting to the local standards.

Companies - Chainalysis, Elliptic

Opportunity - Tailor compliances for emerging markets

Market Makers & Exchanges:

The provide liquidity, price stability and access to stablecoins. Annually trading volume of stablecoins stands at ~$25T. These market makers and exchanges generate liquidity in the market, stabilise the peg and increases the adoption. Centralized Exchanges (CEX) dominate the retail adoption while Decentralized Exchanges (DEX) dominate institutional adoption.

The market is fragmented by geography and product. These firms earn money through trading fees and derivative products.

Companies - Binance, Coinbase, Aave

Opportunity - Specialised infrastructure for stablecoin foreign exchange.

User Interface: The Web 2.0 kind of world for users

On & Off Ramps:

These facilitate the conversion of fiat currency to stablecoins (on ramps) and the conversion of stablecoins to fiat (off ramps). This is the bridge between traditional finance and the crypto world. Without ramps, cryptos would be a closed ecosystem.

Currently, the ecosystem is very fragmented & regionally focused.

Companies - Ramp, Bridge (Acquired by Stripe)

Opportunity - Regional last mile access (remittances, payroll, e-commerce)

Wallets:

This is the interface used for storing, sending and receiving stablecoins. This is also the interface used to pay/ settle bills with merchants in the DeFi ecosystem. Thus, wallets act as the front-door for users.

There are 100M+ wallets globally with a consistently growing Enterprise B2B wallet infrastructure. The key factor in wallet adoption is the compliance and the user experience.

Companies - Metamask, Fireblock, Coinbase Wallet

Opportunity - Niche wallets for freelancers etc.

Decentralised Finance (DeFi):

DeFi is the financial engine where people lend, pay, invest in the crypto ecosystem. $120B+ worth Total Value Locked (TVL - total value of all crypto assets that are deposited, staked, or otherwise locked in DeFi applications) with >50% in stable coins. DeFi is where the capital efficiency kicks in.

Companies - Uniswap, Curve

Opportunity - Regulated money markets on chain

The opportunities I listed under each value chain element is just representative. I would prefer you to first understand how stablecoins work, then understand the various parts of the value chain in details and then come up with potential opportunities yourselves. It’s an almost greenfield with next to impossible in terms of execution ideas.

The other side of the coin & macroeconomics

Stablecoins have been a new life in 2025 through the passing the GENIUS Act which has made landmark progress in legitimizing stablecoins as a form of currency. Let me first list down the key factors at play:

Defines stablecoins as a form of currency and not an investment

Allow private entities to create these coins. Two kinds of companies defined - Non-borrowing entities (eg. Amazon or Walmart) and Insured Deposit Institutions (Traditional Financial Institutions)

Pecking order of bankruptcy has depositors first which gives them confidence

But things aren’t all rosy. The concentration of the stablecoin primarily in the US leads to some major issues that the world and entrepreneurs alike need to be wary of:

Risk of Run on Coins: While the GENIUS Act shores up consumer confidence by placing depositors first in a bankruptcy scenario, it doesn't eliminate the fundamental risk of a digital bank run. The Silicon Valley Bank (SVB) collapse in 2023 was a stark reminder of how quickly confidence can evaporate in the digital age. A similar scenario for a stablecoin issuer is a constant possibility. Imagine a crisis of confidence in a major issuer, perhaps triggered by a rumor about their reserves or a broader market panic. Millions of users could rush to redeem their stablecoins for real dollars simultaneously. The issuer would be forced to sell its T-bill holdings en masse to meet redemption requests. Such a fire sale could potentially force them to sell assets at a loss and causing the stablecoin's value to fall below $1. While the system is designed to be robust, the speed and scale of a digitally-native bank run remain a significant systemic risk.

Dollarization 2.0: Perhaps the most significant geopolitical impact is the acceleration of global dollarization. Stablecoins enable a new, permissionless, and bottom-up version of this phenomenon: Dollarization 2.0. Anyone with a smartphone in a country with a weak or inflating currency can now seamlessly convert their local money into a dollar-denominated stablecoin like USDC thus throttling dollar as the dominant currency for global and domestic trade.

The Threat to Monetary Sovereignty: This citizen-led flight to digital dollars poses a direct threat to the monetary sovereignty of other nations. A central bank's primary power lies in its ability to control the money supply, set interest rates, and manage its economy through its national currency. When a significant portion of an economy begins to transact and save in USDC, the local central bank loses its grip. Its monetary policy tools become less effective because they don't apply to the growing "crypto-dollar" economy. This echoes the historical example of Argentina's currency board in the 1990s, which pegged the peso 1:1 to the U.S. dollar. While it initially crushed hyperinflation, it also meant Argentina effectively outsourced its monetary policy to the U.S. Federal Reserve. When economic shocks hit, Argentina couldn't devalue its currency to remain competitive, ultimately leading to a catastrophic economic collapse. Stablecoins could create a de facto version of this peg, not by government decree, but by popular choice, with similarly challenging consequences for national economic management.

I have consistently ignored the Web 3.0 hype over the last 5 years but stablecoins are no longer just a crypto side story, they are the potential financial rails of the internet. By bridging real-world assets with digital systems, they are addressing inefficiencies that have long held back cross-border trade, remittances, and global commerce.

As regulation brings legitimacy and adoption scales, the question isn’t if crypto-currencies will matter, but how they will be integrated - as private tokens, government-issued CBDCs, or a mix of both. For founders, investors, and regulators, this is an inflection point. Opportunities are plentiful but implementation comes with unprecedented challenges. No one knows where value will be created, all we know is that there will be a wave of wealth creation that will leave behind many corpses with some ultra-winners.

Sign-up to my newsletter

I talk about start-up, investing, tech and everything around it. Sign-Up for my weekly newsletter to never miss an update