India is the largest financial opportunity in the world and also one of the easiest markets to misunderstand. For the last decade, fintech in India looked deceptively simple. If you put a loan button on a phone, or a QR code in a shop, you won. Distribution was scarce, regulation was forgiving and “being digital” itself was the moat. That era is over.

In 2026, India’s financial system runs on public rails. Payments, identity, data sharing, and credit protocols are no longer private advantages — they are government-backed infrastructure. Theoretically, anyone can launch a fintech product but almost no one can build a durable fintech business.

The core mistake investors make today is judging Indian fintech the same way they judge Silicon Valley software—by product quality, early traction, or the promise of Generative AI. While the market fixates on how AI will revolutionize service and distribution, this thesis posits that the fundamental taxonomy remains invariant. AI serves as industrial leverage to improve margins, but it cannot fix a business structure that is fundamentally incoherent.

This thesis starts from a simple belief, in India, the key to fintech success is engineered first and then marketed. On Day 1, a winning company is not defined by what it sells on the surface, but by three deeper questions:

What are you structurally? Are you taking balance sheet risk, selling software, or running critical infrastructure?

What human job are you doing? Moving money, storing value, borrowing, investing, or managing compliance — each comes with a very different regulatory ceiling.

How do you win? In a world of open rails and commodity products, what creates real defensibility?

This thesis proposes a clear framework to answer those questions and an evaluation engine to filter signal from noise. The primary utility of this document is negative selection. It is not designed to guarantee alpha or predict the next outlier (the next CRED); rather, it is built to help you quickly pass on the 90% of deals that are structurally flawed (the "bad CREDs"). It provides the taxonomy to categorize fintechs easily and the logic to kill bad ideas efficiently.

The conclusion is uncomfortable but clear:

Convenience that doesn’t solve psychologically urgent desires (greed or fear) or aren’t fundamentally complex are typically unscalable.

Generic systems in lending, payments, or “AI advice” are structurally fragile.

The regulator is not anti-innovation — but it is brutally intolerant of models that burn retail capital.

The real money in Indian fintech has moved to hard problems:

Deep infrastructure that banks depend on but cannot easily replace.

Deep specialization where startups understand a customer’s reality better than any large institution.

Regulatory moats where compliance friction itself becomes the defense.

This document is not a market map or a trend report. It is a tool designed to help investors and founders judge whether a fintech company is built to last in India.

How to read the report?

This is not a report to read end-to-end like a book. It is a thinking tool. Use it the way you would use a mental model - to test ideas, not to memorize frameworks.

Step 1: Start with the Framework, not the examples

The first section lays out the 3-layer model. This is the core of the thesis. If you understand how Entity, Job, and Playbook fit together, you can evaluate almost any Indian fintech without a deck.

Step 2: Run one startup through it in your head

As you read, pick a real company you know and mentally map it to the framework. Most breakdowns become obvious very quickly.

Step 3: Use the Evaluation Engine as a kill switch

The four-phase evaluation is designed to eliminate ideas, not justify them.

Step 4: Read the case studies for pattern recognition, not picks

The investment theses are worked examples showing how the framework behaves when the pieces actually fit.

Step 5: Treat regulation as a first-order variable

Do not skim the regulatory sections. In India, regulation is not a constraint at the edges - it is the terrain. Every outcome in this report flows from that assumption.

If this report feels reductive at times, that is deliberate. Clarity in Indian fintech comes from subtraction, not addition.

Introduction: The State-Architected Market

India's financial services landscape is a perpetual opportunity shrouded in complexity. The market is opaque, fast-moving, and uniquely "state architected."

Any founder or investor who evaluates an Indian fintech startup on Product-Market Fit alone is ignoring the fundamental forces that dictate success or failure. They are, in effect, mis-pricing risk.

The problem is that our current analysis is siloed. Regulatory analysts discuss compliance; technologists discuss the India Stack; business analysts discuss models. They are speaking different languages about the same company. The primary purpose of this thesis is to establish a Common Taxonomy. To successfully invest in 2026, we need a unified language - one that captures the physics of the business, the utility to the user, and the strategic edge over the incumbent in a single view.

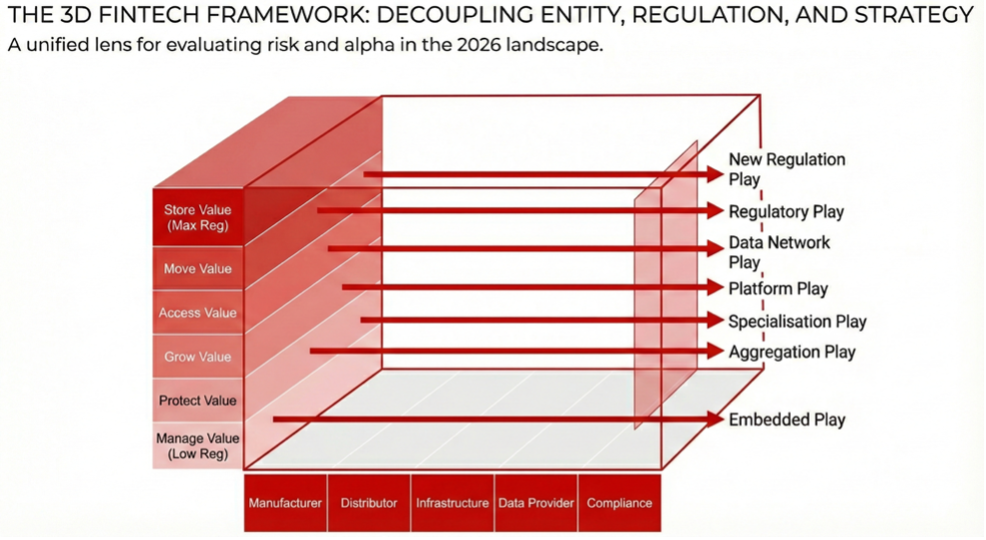

The 3D Framework

This thesis introduces a comprehensive framework for VCs and founders to dissect opportunities. It operates on the premise that a fintech is not just a company, but an entity that must simultaneously navigate three distinct, interconnected layers:

Layer 1: The Entity (The DNA): What are you structurally? Are you a Manufacturer taking balance sheet risk, or an Infrastructure provider selling rails? This layer dictates your P&L structure, capital efficiency, and valuation ceiling.

Layer 2: The Job to Be Done (The Utility): Why do you exist? Which fundamental human need are you solving (Move, Store, Borrow, Grow, Insure, Verify)? In India, the "Job" dictates your regulatory complexity and the supervision intensity you will face.

Layer 3: The Strategic Playbook (The Edge): How do you win? In a market of commoditized products and open rails, your "Playbook" is your mechanism for defensibility. It is how you navigate the chessboard better than the competition.

The Objective

The aim is to move beyond the product demo or the founder story and into a systemic analysis of advantage. We are looking for:

Structural Compounding: Business models where the Entity structure (Layer 1) aligns perfectly with the Regulatory ceiling (Layer 2).

DPI-Native Leverage: Playbooks (Layer 3) that utilize public rails (like AA or OCEN) to do things previously impossible for private companies.

Regulatory Moats: Where the friction of the "Rulebook" creates a defensive wall against incumbents and tourists.

This document is a tool. It is designed to be an Evaluation Engine. Use The Framework to grade the physics of the business, and The Evaluation Flowchart to validate the investment thesis.

The FinTech Framework

In the early phases of Indian Fintech (2016–2020), value was created simply by providing Access. If you could put a loan button on a phone or a QR code at a shop, you won. The market was starved for digitization, and "being digital" was the moat. In 2026, that era is over.

With the maturity of Digital Public Infrastructure (UPI, AA, ONDC, OCEN), the "rails" of financial services have in essence become public goods. Access is now commoditized. A startup can no longer generate alpha simply by being a lender or being a payment processor. When the cost of distributing a financial product approaches zero, the "What" becomes less important than the "How."

To evaluate a fintech startup in this mature landscape, we must stop confusing the Product with the Playbook.

This thesis proposes a new taxonomy for Indian Fintech. To understand any opportunity, we must decouple the startup into three distinct layers. This framework allows us to separate the company's DNA from its strategic edge.

The 3D Fintech Framework

Layer 1: The Entity (Value Creation)

What are you structurally?

This is the most critical question for a founder or a VC. Layer 1 defines the P&L structure, the regulatory cost, and the valuation ceiling. A "Lending Tech" company and a "Lender" might look the same on an app store, but they are fundamentally different species – it defines what risk you hold. We classify every financial services player into 5 types of entities:

Infrastructure Provider:

The Monopolist - They provide the rails or API on which other financial services players build their business. This is the most brutal business to start, but the most defensible if you win. It is a Trust Game. You are processing mission-critical flows (Payments, Account Aggregation, KYC) for regulated entities.

Tech Margins, Regulatory Liability: You enjoy the gross margins of a SaaS company, but you carry the existential risk of a bank. One major slip (downtime or fraud), and you are evicted.

The Monopoly Imperative: The market naturally consolidates into a monopoly-esque, winner takes most structure. Distinct leaders emerge for specific segments (e.g., Razorpay for Startups/SaaS vs. Cashfree for Marketplaces). There is no prize for third place.

Product Manufacturer:

The Fulcrum - They are the actual "factory" in the traditional sense. Whether it is an NBFC creating a loan, an Insurer underwriting a policy, or a platform like Smallcase creating a basket of stocks - they manufacture the financial asset. The entire ecosystem exists only because they exist.

Being the manufacturer does not guarantee you keep the profit. Just as Foxconn manufactures the iPhone but Apple (the brand/distributor) keeps the margin, in finance, the Manufacturer often bears 100% of the balance sheet risk while the Distributor or Data provider eats the cream.

The Moat: Capital and Licensure. It is brutally hard to build a factory. You need the deepest regulatory licenses and massive capital buffers. This creates a high floor, but the ceiling depends on your distribution power.

Product Distributor:

The Aggregator of Choice - These entities are purely focused on distributing products that other entities have manufactured. An insurance comparison platform like Ditto is a distributor while the actual insurance company is the manufacturer. Manufacturers (like Banks or Insurers) are inherently limited, they can only sell their own products. Customers, however, demand choice. The Distributor wins by becoming the "Multi-Brand Outlet" (MBO) for finance.

The Moat of Comparison: A Manufacturer (e.g., Shivalik SFB or ICICI Lombard) cannot displace a Distributor (e.g., Stable Money or Ditto) because they cannot offer an unbiased comparison. A customer wants to compare HDFC Ergo against ICICI Lombard before buying. One of the Distributor’s moat is neutrality.

The Moat of Knowledge Generation: The manufacturer typically is too bogged up with the technicalities of building the actual product to educate their buyers. Finance products need more educating to sell because of lack of financial sophistication in the general public. Thus, a Ditto also acts as the knowledge source for the buyer, helping them understand the choice rubric for their evaluation.

The Value Add: It is not just "lead generation." The alpha lies in reducing friction in "hard-to-access" markets. Example: Stable Money didn't just sell FDs; they aggregated a fragmented market that banks individually couldn’t digitize. Ditto didn't just sell insurance - they turned a complex, spam-filled process into a 2-minute advisory flow.

Data Provider:

The Silent Power - The entire BFSI sector runs on data. Data Providers are the silent layer powering every firm. High-quality data in India is neither free nor cheap.

Real-time market data from BSE/NSE can cost upwards of ₹30-40 Lakhs/year. Players like Accord FinTech or Refinitiv command immense pricing power because they control the feed.

It isn't just raw pipes. It is also the "Reporting Layer" (e.g., MProfit). The entity that can ingest raw chaos and output clean, tax-ready reports becomes the sticky operating system for the user.

Compliance Provider:

The Shield - Compliance in India is a "Tax" on existence. It is volatile, complex, and mandatory. These are entities that provide compliance-as-a-service.

The Moat of "Bandwidth": Why do banks pay external vendors for KYC or Consent Management? Not because they can't build it, but because they don't have the bandwidth to maintain it.

A Compliance Provider monetizes the "Headache." They track the ever-changing RBI or SEBI circulars so the client doesn't have to. You are paying them to keep your license safe while you focus on your product.

Different entity types and their valuation ceilings

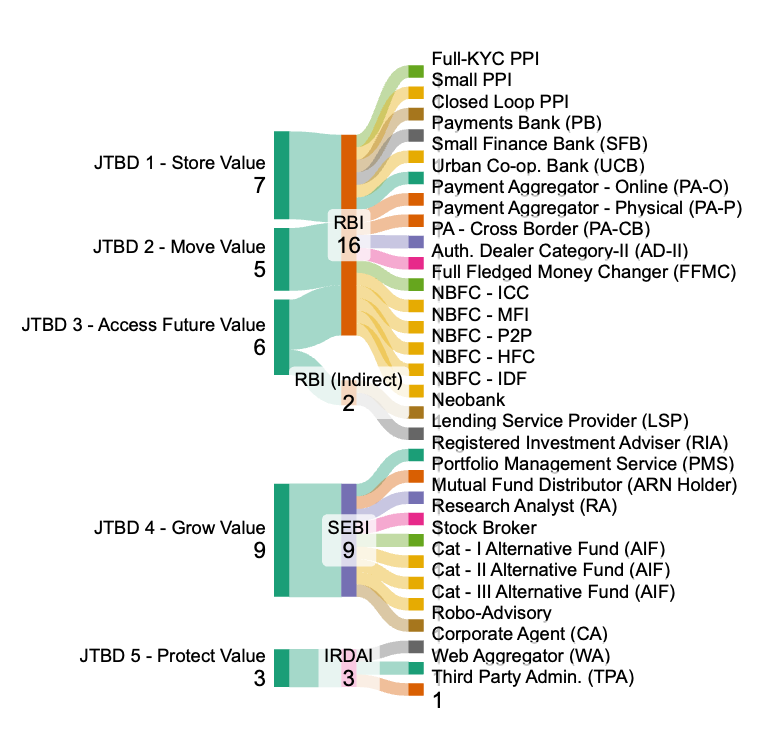

Layer 2: The Job to be Done (Demand)

Why do you exist?

While Layer 1 defines who you are, Layer 2 defines what you solve. In India, the "Job" directly correlates to the "Regulatory Ceiling" and the intensity of supervision you will face. We’ve defined 6 key utilities in financial services:

Store Value

Banking, deposits, wallets

This category is defined by entities that can legally hold customer funds. The broad regulatory difference is all about what you can do with the deposit.

Regulatory Ceiling: The RBI is paranoid about deposit safety. Only Banks and licensed PPIs (Prepaid Instruments) can play here.

The License Trap: Securing the license is only 10% of the battle. Retaining it is the war. As seen with the Paytm Payments Bank saga, the regulator now demands "Bank-Grade" compliance even from tech-first players. There is no "Move Fast and Break Things" when you hold the user's principal.

The Walled Garden: You cannot touch the money without a direct license. Neo-banks are merely UI-wrappers (Distributors) sitting on top of a licensed bank's ledger.

Move Value

Payments, remittances

This category is for entities that facilitate the movement of money but do not (typically) hold it overnight.

Regulatory Ceiling:High (Operational). Regulators care about AML (Anti-Money Laundering) and Fraud. They don't care if you lose money, but they care if you move dirty money.

Constraint:The PA License Cap. The RBI's "Payment Aggregator" (PA) license has become the new barrier to entry. Without it, you are dependent on another infra player, compressing your margins to near-zero.

Key Constraint: Zero-MDR (Merchant Discount Rate) on UPI has killed revenue here. Value must be found in cross-border remittances or other non-UPI workflows (eg. complex B2B flows)

Access Value

Credit & lending

This category includes entities that lend money from their own balance sheet or facilitate lending for others. Lending is easy, collecting is hard. Regulation changes based on source of capital.

Regulatory Ceiling:Complex. Regulation changes based on the Source of Capital (Bank vs. NBFC vs. P2P).

End of FLDG: The "First Loss Default Guarantee" (FLDG) used to be the magic wand that let fintechs act like banks. The RBI has capped this at 5%. This forces Fintechs (LSPs - Loan Service Providers) to either build true underwriting tech that banks trust blindly or become mere lead-gen agencies for the banks.

Constraint:Digital Lending Guidelines (DLG). The DLG mandates that money must flow directly from the Bank to the Borrower, cutting the Fintech out of the flow of funds. You can't skim the float anymore.

Grow Value

Wealth & investments

Regulation driven by level of decision-making authority, risk level of investment asset & investment corpus

Regulatory Ceiling:Fiduciary. SEBI rules distinguish sharply between Advice (RIA - strict) and Distribution (Broker/Agent - looser).

The "Advice Gap": SEBI's strict fee caps and compliance norms for RIAs make "Pure Advice" unscalable for the masses. There are only 991 RIAs for a 1.4B population as of December 2025. This creates a market failure - Consumers need advice but won't pay for it, they only pay commissions (hidden in products).

Constraint:Execution vs. Advice. You cannot be both the Doctor (Advisor) and the Pharmacist (Distributor). Startups must choose one path, limiting monetization flexibility.

Protect Value

Insurance & risk

This category includes entities that distribute or service insurance policies.

Regulatory Ceiling:Prescriptive. IRDAI dictates product structures and commission caps.

Distribution is the Moat: Since product structures are standard and pricing is regulated, the only alpha is in Distribution Efficiency.

Constraint:Capital Intensity. Manufacturing insurance requires massive capital reserves (Solvency Ratio). Web Aggregators face strict limitations on "claims repudiation" - they can sell the policy, but they can't control the claim experience, which is the core product.

Manage Value

The Job: Identity, privacy, compliance, and treasury control.

Regulatory Ceiling: Often regulated via the DPDP Act or as a TSP (Tech Service Provider) to a regulated entity.

Liability often flows down from the regulated partner and not the player offering compliance as a service.

Constraint:The "Cost Center" Stigma. Companies in this space struggle to prove ROI. You are a grudge purchase, bought only to avoid a fine.

This is where the Alpha lies. In a market where Layer 1 (Entity) is a choice of "Risk vs. Scale" and Layer 2 (JTBD) is a choice of "Regulator," Layer 3 is the only true canvas for innovation. It defines how you compound advantage.

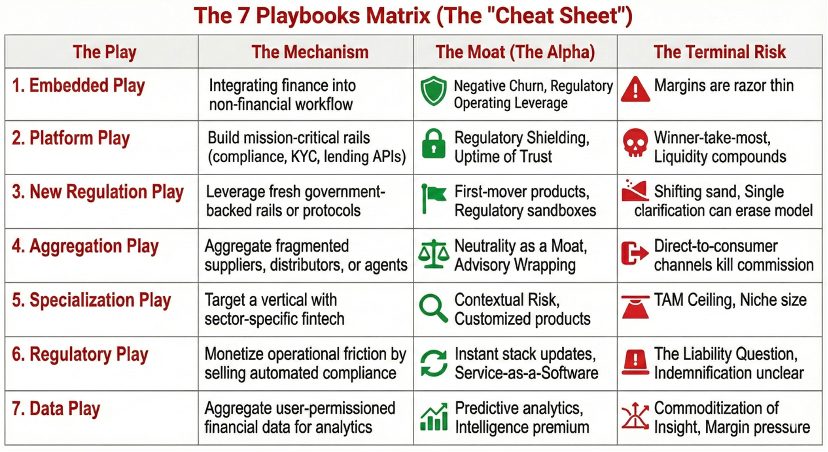

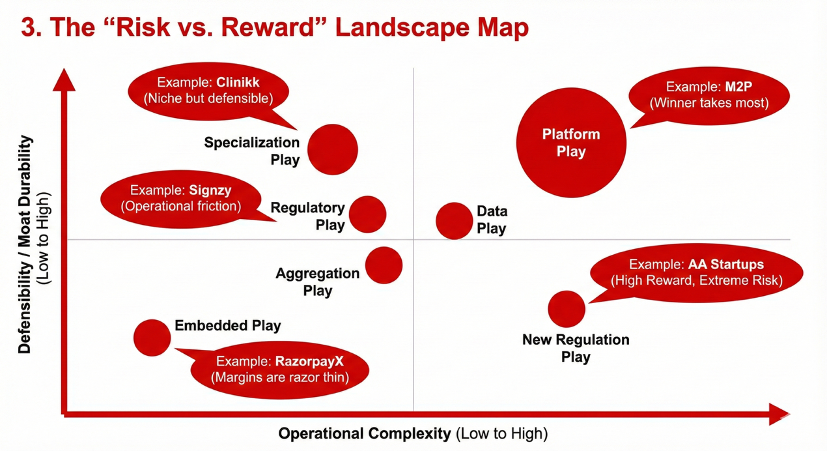

In 2026, a startup wins not because it is a "Lender" (Layer 1) solving "Access" (Layer 2). It wins because of the Playbook it uses to defend its margins. There are 7 Strategic Playbooks available to Indian founders. These are not mutually exclusive; the strongest companies often stack them:

Embedded Play

Integrating finance into non-financial workflow. Integrate financial services directly into the user’s core workflow, making payments, credit, or insurance a feature - not a standalone destination.

Example: RazorpayX embeds business banking and payouts into payroll and vendor management SaaS, so finance happens invisibly within business operations.

The Churn-Killer: In 2026, Embedded Finance is not a revenue strategy, it is a retention strategy. The "Take Rate" on payments or loans is razor-thin and shared with the bank. The real value is that a SaaS platform with embedded banking has Negative Churn. It is operationally painful for a customer to switch their "Operating System" once their money flows through it.

The Moat:Regulatory Operating Leverage. The cost of compliance (LSP norms, FLDG caps) is a fixed cost. Only large SaaS players can amortize this across millions of users, effectively locking out smaller, niche Fintechs.

Platform Play

Build the mission-critical rails - compliance, KYC, lending APIs, payment gateways - used by regulated entities and platforms to deliver financial products.

Example: M2P Fintech provides card-issuing, payment processing, and lending APIs as backend infrastructure for consumer neo-banks and traditional banks.

Trust & Governance: It’s not about the API; it’s about the "Uptime of Trust." Banks don't buy M2P because they can't write code, they buy it to offload the headache of regulatory flux. The Infra player sells Regulatory Shielding wrapped in an API.

The Terminal Reality: This is a "Winner-Take-Most" market. Liquidity and reliability compound. There is no space for the 4th best Payment Gateway. This leads to massive valuations for the leader and death for the rest.

New Regulation Play

Leverage fresh government-backed rails or compliance protocols to launch first-mover products and test them inside regulatory sandboxes.

Example: Account Aggregator (AA) startups build unified data retrieval and consent management platforms as soon as RBI regulations and Sahamati protocol go live.

Pioneer's Penalty vs. Prize: The first mover often dies clarifying the rules (regulatory friction). The winner is usually the "Fast Follower" who enters after the circulars stabilize but before the banks build it in-house. That is not the de-facto outcome, but is a high-potential possibility.

Terminal Risk: You are building on shifting sand. A single clarification from the Regulator can erase the business model overnight (e.g., the ban on non-bank PPI loading).

Aggregation Play

Aggregate fragmented suppliers, distributors, or agents into a unified platform, simplifying discovery, onboarding, and compliance at scale.

Example: Fintso aggregates thousands of mutual fund distributors, providing digital portfolios, compliance automation, and investor analytics.

Neutrality as a Moat: In a world of Manufacturer-owned apps (e.g., an HDFC Bank app selling only HDFC), the customer craves an unbiased referee. The Aggregator wins not by having more supply, but by having better comparison tools.

Pure listing is dead (Google does that). The alpha is in Advisory Wrapping - using data to tell the user what to buy, not just showing them what is available.

Terminal Risk: Large insurers and banks are aggressively building direct-to-consumer channels to kill the aggregator's commission.

Specialization Play

Target a vertical (industry, segment, or workflow niche) and build sector-specific fintech, such as healthcare payments or SME insurance with tailored underwriting.

Example: Clinikk is a healthtech fintech that combines insurance, health subscriptions, and payments for the medical sector.

Context is King: A generic bank sees a "Credit Score." A specialized player sees "Cash Flow." By owning the workflow (e.g., the doctor’s clinic management software), the startup understands the user's risk profile better than any lender.

Customized Risk: The ability to create bespoke products (e.g., "Waiting Room Insurance" or "Inventory Finance" based on real-time stock) that generic banks simply cannot underwrite.

Terminal Risk: The TAM Ceiling. Is the niche big enough to support a venture-scale outcome? Many specialization plays end up as great SME businesses but poor VC returns.

Regulatory Play

Monetize operational friction by selling automated compliance, KYC, AML, consent orchestration, or auditing as a service for banks and NBFCs.

Example: Signzy automates KYC and AML onboarding, video liveness checks, and document verification for regulated entities across India.

Service-as-a-Software: Before AI, this was "Service-as-a-Software." Financial Service players pay this "tax" not because they can't do KYC, but because they lack the bandwidth to maintain it. The moat is the ability to update the stack instantly whenever a new circular drops.

The Liability Question. The existential question for 2026: Does the startup take the blame? If a KYC fails and fraud happens, will the bank indemnify the vendor? The market has no clear answer yet.

Data Play

Aggregate user-permissioned financial data for analytics, underwriting, credit scoring, or product personalization, aligning with AA or DPDPA standards.

Example: Perfios uses account aggregator and consented data to build advanced credit analytics and real-time financial health scoring for lenders.

Commoditization of Insight: As AI models become cheaper, the "intelligence premium" drops. The data provider must constantly move up-stack to predictive analytics to maintain margins.

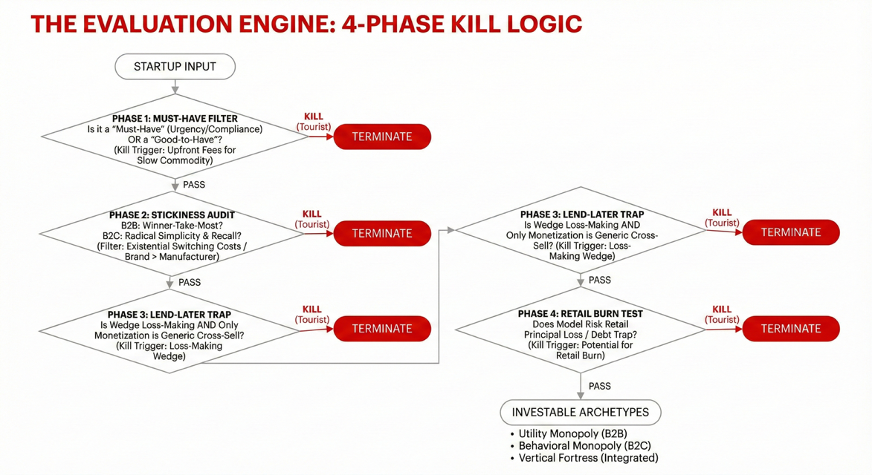

The Evaluation Engine

Investing in Indian Fintech is not only about finding the "best product." It is about finding the coherent stack.

A startup is coherent only when its Entity structure (Layer 1) can survive its Regulatory Ceiling (Layer 2) using a specific Strategic Playbook (Layer 3).

But coherence is just the baseline. To identify the outliers, we need to strip away the pitch deck vanity metrics (GMV, Downloads) and stress-test the business against the harsh realities of the Indian market.

We use a 4-Phase Exclusion Algorithm. If a startup fails any phase, it’s a Kill.

Phase 1: The "Must-Have" Filter (Utility vs. Monetization)

The Premise: "Convenience" is a public good in India (UPI, DigiLocker). You cannot charge for what the government gives for free.

The Filter: Does the product solve a need that is either psychologically urgent (Greed/Fear) or structurally complex (Compliance)?

The "Inconvenience Paradox":

The Trap: Some sectors are highly inconvenient but impossible to monetize. An "AI Mutual Fund Advisor" solves a real pain point, but the Indian consumer views advice as a free commodity. It is a "Good-to-Have." Verdict: PASS.

The Exception: An "AI F&O Trader" is also just convenience, but users pay for it because of the psychological pull of minting money. It shifts from "Utility" to "Greed." Verdict: INVEST.

The Monetization Reality:

Direct Charge: Only works if the "Cost of Non-Compliance" is higher than the fee (e.g., ClearTax). If you charge ₹500 for a "Financial Health Report," you die.

Hidden Rail: If the product is free, the monetization must be unbiased. If a "Free Advisor" pushes high-commission junk policies, they are a Distributor masquerading as a Product. The regulator will eventually sniff this out.

The Monopoly Bet: Loss-leading utility (like CRED) only works if the "Addiction Horizon" is visible. You are betting that 10 years from now, the user is so hooked they cannot leave. This is a Venture Bet, not a Business Bet.

💡

The Kill Trigger: Charging upfront fees for a "slow growing" commodity need (e.g., Generic Advice) from Day 1.

Phase 2: The "Stickiness" Audit (Right to Win)

The Premise: Every founder claims a moat. In early-stage fintech, "Read/Write" access is a weak metric. Stickiness comes from Market Structure (B2B) or Radical Simplicity (B2C).

The Filter:

For B2B: The "Winner-Take-Most" Test

It’s not about the software; it’s about becoming the Standard.

Accord FinTech charges lakhs for data because they are the "Bloomberg" of their niche. M2P creates stickiness not just via code, but by pricing compliance infrastructure so efficiently that undercutting them is mathematically impossible.

The Question: Is the cost of ripping this out existential for the client?

For B2C: The "Recall" Test

Distribution is dispensable. Simplicity is the moat.

Google Pay beat BHIM not on tech, but on UI. Paytm lost ground when it became a complex Super App.

The Question: When the user thinks of the category (e.g., "Credit Card Bill"), do they think of the App (CRED) or the Bank? If the App has Brand Recall > Manufacturer, they have a Right to Win.

Phase 3: The "Lend-Later" Trap (Profitability)

The Premise: Cross-sell is a retention strategy, not a monetization strategy.

The Filter:

The History Lesson: Razorpay didn't start lending in Year 2. They spent a decade building the definitive payments layer. Lending was a retention tool to stop merchants from churning, not a desperate pivot for revenue.

The Hard Truth: If the "Wedge" product (Payments/SaaS) is loss-making and the only path to profitability is "We will lend to them in Year 3," the model is broken.

The Only Exception:Deep Vertical Integration. A "Vertical SaaS for Hospitals" (e.g., Clinikk) can lend because it owns the entire workflow (EMR, Appointments, Payments). Here, lending is a feature of the workflow, not a blind bet.

💡

The Kill Trigger: Wedge is Loss-Making AND the only Monetization Plan is "Generic Cross-Sell."

Phase 4: The "Retail Burn" Test (The Regulatory Vector)

The Premise: The Regulator is not a monolith. The RBI has a single "God Metric": Retail Protection.

The Filter: We don't look for "Legal vs. Illegal." We look for "Benign vs. Predatory."

Gray Zone + Retail + High Risk: (e.g., Unregulated P2P, Crypto Speculation). If a retail user can lose their principal or get trapped in debt → KILL. The regulator will shut this down.

Gray Zone + Retail + Low Risk: (e.g., Tax Optimization, Insurance Advice). If the model helps financialization and the downside is low → INVEST. The regulator wants this to exist.

Gray Zone + B2B: (e.g., Treasury Management). The client is sophisticated enough to do due diligence. INVEST.

💡

The Kill Trigger: Is there a potential for the retail participant to burn their hands? If yes, the business has a terminal date.

The Decision Flowchart

The Output: The Decision Matrix

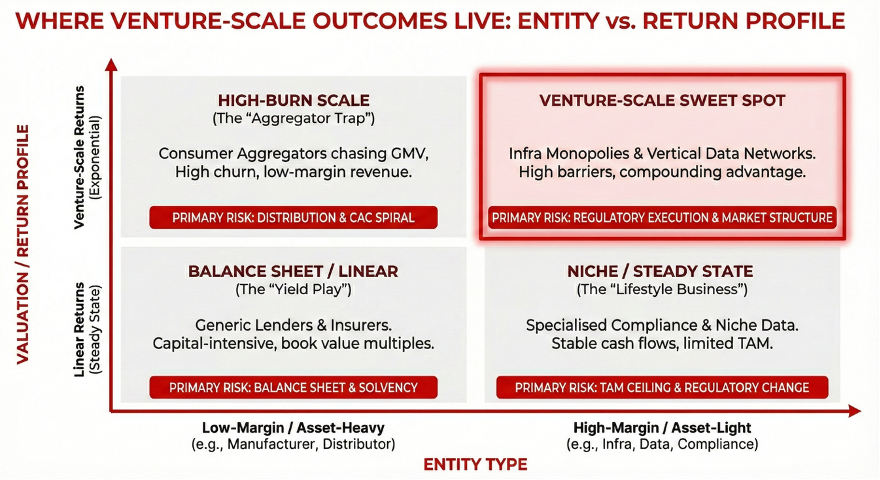

If a startup survives the 4-Phase Audit, it is not just "good" - it is coherent. But not all coherent startups are equal. In 2026, we only write checks for three specific archetypes.

The "Utility Monopoly" (The B2B Bet)

The Profile: Infrastructure or Data providers (Layer 1) solving a "Must-Have" complexity (Layer 2) via a Platform Play (Layer 3).

The Thesis: You are betting on Market Structure.

The Winning Trait:"Existential Switching Costs."

Example:Accord FinTech. You don't buy it because you love it; you buy it because running a brokerage without it is impossible.

The Vibe: Boring, high-margin, unkillable.

The "Behavioral Monopoly" (The B2C Bet)

The Profile: A consumer app solving "Move/Grow" (Layer 2) via a radical Simplification or Rewards loop.

The Thesis: You are betting on Psychology (Greed, Fear, or Status).

The Winning Trait:"The Addiction Horizon."

Example:CRED or F&O Platforms. They don't just solve a problem; they create a habit. You invest knowing the "Monetization Rail" might be hidden today (Loss Leader), but the "Recall" is so absolute that pricing power is inevitable.

The Vibe: Polarizing, high-burn, massive potential outcome.

The "Vertical Fortress" (The Integrated Bet)

The Profile: A specialized player (Layer 3) owning the entire workflow of a niche sector (Layer 2).

The Thesis: You are betting on Context.

The Winning Trait:"Write Access."

Example:Clinikk. They don't just "Read" the doctor's data; they "Write" the prescription and the bill. Because they own the "Moment of Truth," they can monetize via Credit/Insurance where generic players cannot.

The Vibe: Hard to build, slow start, exponential retention.

Investment Thesis Pick 1: The B2B Stablecoin NeoBank

The What (The Alpha)

The Idea: A Vertical Neobank for Indian Service Exporters (Dev Agencies, SaaS, Freelancers) that runs on Stablecoin Rails (Backend) but functions like a Fiat Bank Account (Frontend).

The Problem:

The "SWIFT Tax": Indian exporters lose 3–4% of revenue to opaque FX spreads and wire fees. For a low-margin agency, this wipes out ~30% of net profit.

The "FIRC Nightmare": Receiving money is easy; proving it is tax-exempt is hell. Banks take 5–7 days to issue the FIRC (Foreign Inward Remittance Certificate). Without this, the exporter faces a flat 18% GST hit.

Why Now (The 2026 Unlock):

Regulatory: The RBI’s PA-CB (Payment Aggregator - Cross Border) license finally legalizes non-banks holding and processing these export flows.

Structural:GIFT City (IFSCA) now allows "Dollar-Denominated Accounts" for B2B use, creating a legal bridge to hold/convert Stablecoins (USDC) before off-ramping to INR.

The 3-Layer Analysis (The Structure)

We decouple the startup to ensure the stack is coherent.

Layer 1: The Entity (Distributor with Infra Characteristics)

Structure: Legally a Distributor (Partner to AD-1 Bank).

The Twist: Unlike generic neobanks, it owns the "Compliance Layer" (FIRC generation). It sells software, but the stickiness is akin to Infrastructure.

Layer 2: The Job to Be Done (Move Value + Manage Value)

Primary Job: Move Value (USD Client to INR Account).

Regulatory Ceiling: High. Requires PA-CB + FIU Registration. The constraint is AML, not Solvency.

Layer 3: The Strategic Playbook (New Reg + Specialization)

Play 1: New Regulation Play. leveraging the PA-CB license to breach a fortress previously held by banks.

Play 2: Specialization Play. By focusing only on Service Exporters, the startup automates specific "Purpose Codes" and FIRC tagging that generic banks handle manually.

The Evaluation Audit (The 4-Phase Kill Switch)

Phase 1: The "Must-Have" Filter (Utility)

Question: Is this "Convenience" (Nice to have) or "Capital" (P&L Impact)?

Verdict: CAPITAL.

Saving 3% on FX is not a convenience; it is immediate EBITDA expansion.

Monetization: Day 1 Profitable. The startup charges a ~1% spread (vs. Bank's 3%). The client wins, and the unit economics are healthy. (PASS)

Phase 2: The "Stickiness" Audit (Right to Win)

Question: Is this a "Winner-Take-Most" B2B utility?

Verdict: YES (via Write Access).

A generic "Crypto Exchange" cannot win because they don't solve the FIRC.

The Moat: The "Auto-FIRC" engine writes compliance proof directly into the client’s ERP (Zoho/Tally). Once integrated, the switching cost is existential—leaving means returning to manual paperwork. (PASS)

Phase 3: The "Lend-Later" Trap (Profitability)

Question: Is the Wedge loss-making?

Verdict: NO.

Cross-border payments have a natural 0.5% - 1% Take Rate.

The startup generates cash from the first transaction. It does not need to "Lend Later" to survive (though it can lend against invoices to compound revenue). (PASS)

Phase 4: The "Retail Burn" Test (Regulatory Vector)

Question: Is this a "Predatory Gray Zone"?

Verdict: MAYBE (Binary Risk).

Risk: Using Stablecoins in the backend is a gray zone. RBI either regulates this or bans it.

Mitigation: The Client (Exporter) never touches the Crypto. They send USD, receive INR. The platform manages the volatility and custody.

Final Grade: The Utility Monopoly

This is a High Conviction bet. It solves a P&L problem, monetizes immediately, and uses a Regulatory Moat (PA-CB) to defend against Tourist fintechs.

Investment Thesis Pick 2: P2P Lending 2.0

The What (The Alpha)

The Idea: A specialized NBFC-P2P platform connecting Retail Lenders not to "Random Borrowers" (Personal Loans), but to "Blue-Chip Supply Chains" (Invoice Discounting/Vendor Finance).

The Problem:

The SME Gap: An SME Supplier to Unilever/Tata waits 90 days for payment. Banks reject them for working capital due to lack of collateral (Real Estate).

The Yield Crisis: Indian middle-class capital is starving. FDs yield ~7% (post-tax ~5%), losing to inflation. Retail investors are chasing dangerous assets (F&O, Crypto) to find yield.

Why Now (The 2026 Unlock):

Regulatory: The RBI’s tightening of P2P norms (banning "pool accounts" and "guaranteed returns") has killed the "Pseudo-Banks." The only survivors are True Marketplaces.

Structural:GSTN + AA Rails. We can now verify a valid invoice from a corporate anchor in real-time, effectively underwriting the Anchor’s creditworthiness, not the SME’s.

The 3-Layer Analysis (The Structure)

Layer 1: The Entity (Marketplace with Manufacturer Constraints)

Structure: NBFC-P2P License.

The Twist: It is technically a "Manufacturer" (Regulated Entity), but financially a Distributor. It holds Zero Balance Sheet Risk. If the borrower defaults, the retail investor takes the hit. This allows infinite ROE (Return on Equity) if managed well.

Layer 2: The Job to Be Done (Access Value + Grow Value)

Primary Job (Borrower): Access Value (Working Capital).

Secondary Job (Lender): Grow Value (Alternative Fixed Income).

Regulatory Ceiling: Complex. The "Radioactive Risk" is Conduct. You cannot promise returns. You cannot touch the money (Escrow only).

Layer 3: The Strategic Playbook (Specialization + Aggregation)

Play 1: Specialization Play. Don't lend to "Everyone." Lend only to "Auto Component Suppliers." You underwrite the Sector Cycle, not just the borrower.

Play 2: Aggregation Play. Aggregating retail capital to fund wholesale needs.

The Evaluation Audit (The 4-Phase Kill Switch)

Phase 1: The "Must-Have" Filter (Utility)

Question: Is this "Convenience" or "Capital"?

Verdict: CAPITAL.

For the SME: It is survival capital (Inventory purchase).

For the Lender: It is Alpha. Earning 11% on an invoice is a "Must-Have" for a portfolio beating inflation.

Monetization: Day 1 Profitable. You charge a spread (e.g., Borrower pays 14%, Lender gets 11%, Platform takes 3%). (PASS)

Phase 2: The "Stickiness" Audit (Right to Win)

Question: Is this a "Vertical Fortress"?

Verdict: YES (via Anchor Integration).

A generic P2P player (like Faircent/LenDen) cannot compete because they lack the data.

The Moat:ERP Integration with the Anchor. If you integrate with the Corporate’s ERP to see "Approved Invoices" in real-time, you have Write Access to the truth. You know the invoice is valid before you lend. A generic player is guessing; you are verifying. (PASS)

Phase 3: The "Lend-Later" Trap (Profitability)

Question: Is the Wedge loss-making?

Verdict: NO.

Lending is the core product. There is no cross-sell hope here.

The unit economics are healthy from the first loan. The risk is Volume (Cost of Acquisition for Lenders), not Margin. (PASS)

Phase 4: The "Retail Burn" Test (Regulatory Vector)

Question: Is this Predatory? (The Critical 2026 Test)

Verdict: INVESTABLE (If Structured Correctly).

The Risk: Unsecured Personal Loans (P2P 1.0) burned retail hands when defaults hit 10%+.

The Shield (P2P 2.0): Short Duration & Secured Nature.

Asset: Invoice (30–90 days). The money comes back fast.

Risk: You are betting on Tata/Unilever paying their bill, not on Ramesh paying his salary loan.

Alignment: The government is desperate to solve the MSME Credit Gap. Channeling household savings into MSME production (via invoices) is the "Holy Grail" of economic alignment. (PASS)

Final Grade: The Vertical Fortress

This is a high-conviction bet because it replaces "Underwriting Risk" (guessing if a person will pay) with "Information Advantage" (knowing a corporate must pay).

Conclusion: The Synthesis

The 3-layer taxonomy is a lens. It does not tell you what to think, it tells you how to look. Here is the honest accounting of what this framework delivers and where it ends.

What This Framework Enables

Faster Deal Killing: The bottleneck in VC is not finding good deals; it is filtering out the noise. This framework creates immediate "Kill Triggers."

If the Wedge is loss-making and the monetization is "Cross-Sell later" → Kill.

If the Regulation is Gray Zone and Retail Capital is at risk → Kill.

You stop wasting weeks on "Tourists" who look good on a slide deck but fail the physics test.

Clearer IC Debates: Most Investment Committee debates are messy because everyone is using different definitions. One partner looks at Growth (Distributor metrics), another looks at Risk (Manufacturer metrics).

This framework forces a Shared Taxonomy.

We stop arguing "Is this a good business?" and start asking "Is this a coherent Infrastructure Play?"

It aligns the team on the Risk Profile before we even discuss the Valuation.

Reduced Regulatory Blind Spots: We stop asking the wrong question ("Is it legal today?"). We start asking the right question ("Is it aligned with the Regulator’s goal of Retail Protection?"). This prevents us from funding "Regulatory Arbitrage" that looks like innovation but has a terminal date.

What This Framework Does Not Do

It Does Not Predict Winners: Coherence is just the baseline. A startup can have a perfect 3-Layer Stack - a sound Entity, a valid Utility, and a smart Playbook - and still fail because of bad execution, founder conflict, or poor culture. The Framework filters out the structurally doomed. It does not guarantee the operationally excellent.

It Does Not Replace Judgment: Venture is an art of people. The "Founder’s Grit," "Sales Ability," and "Vision" cannot be put into a matrix. Use the framework to grade the Business Physics. Use your gut to grade the Founder Physics.

It Does Not Solve Timing: You can be right about the Thesis (e.g., "P2P 2.0 is the future") but wrong about the Time (e.g., the regulation isn't ready yet). Being right too early is the same as being wrong. The framework identifies Structural Viability, not Market Timing.

How This Thesis Should Age

What Breaks If Regulation Shifts? The specifics of the thesis picks (P2P 2.0, Stablecoins) are sensitive to circulars.

If the RBI bans P2P entirely, the P2P 2.0 thesis dies.

If the Govt bans all crypto rails, the Stablecoin thesis dies.

Adaptation: The "Plays" (Layer 3) must evolve, but the core need remains.

What Remains Invariant? The 3-Layer Taxonomy is permanent.

A Manufacturer will always have balance sheet risk.

A Distributor will always rely on CAC/LTV.

"Retail Protection" will always be the Regulator’s God Metric.

Why Structure Outlives Cycles? Markets go up and down. Valuation multiples expand and contract. But the Physics of the P&L do not change.

A business that relies on "Lend-Later" cross-sell to survive is bad in a Bull Market and dead in a Bear Market.

A business with "Existential Switching Costs" is valuable in any cycle.

This framework is built on the belief that while Technology changes every year, the rules of Business Survival are eternal.

The AI Postscript

Does Artificial Intelligence break this thesis? No,It validates it. We view AI not as a new "sector," but as Industrial Leverage that creates new opportunities without altering the fundamental physics of the market.

The Structure Remains Invariant

AI cannot code away a balance sheet risk. It cannot hallucinate a banking license.

A Manufacturer still needs capital buffers.

A Distributor still needs user trust.

The Regulator still prioritizes retail protection above innovation.

The 3-Layer Taxonomy defined in this document is immune to the model weights of GPT-5.

The Opportunity: Service-as-Software

What AI does change is the margin structure. Historically, high-trust businesses (Wealth Advisory, SME Underwriting) were capped by human bandwidth. AI removes this ceiling.

The opportunity for 2026 is to build "Service-as-Software" entities—companies that operate with the trust of a bank but the gross margins of a SaaS company.

The competitive edge has shifted from the Model to the Orchestration of the business. The winner will not be the engineer with the best code, but the operator who uses AI to navigate the regulatory maze faster than the incumbent.

Appendix

The Key Players (The Rule Maker)

Every financial service company answers has to work with the following key players:

Vertical regulator - creates the core regulations for that industry vertical. They own the definition of what constitutes regulated activity in their domain, set capital requirements, and control licensing. Their scope is deep but narrow.

Horizontal enforcers - These agencies don't regulate specific financial activities, but enforce universal, cross-cutting laws that all companies must follow. Their scope is broad but shallow.

Self Regulatory Organizations (SROs) - ****create the "soft law" and operational rules that startups often interact with daily.

Digital Public Infrastructure - These are not enforcers (like FIU) but open, interoperable networks that create new market structures.

Vertical Regulators:

Agency

Core Domain

RBI (Reserve Bank of India)

Banking: Money, Payments, Credit, Banking.

SEBI (Secs. & Exchange Board)

Capital Markets: Investing, Wealth, Stocks, Bonds, Funds.

IRDAI (Insurance Reg. & Dev.)

Insurance: All insurance manufacturing and distribution.

PFRDA (Pension Fund Reg. & Dev.)

Pensions: The National Pension System (NPS) & retirement.

IFSCA (International Financial Services Centres Authority)

It acts as a unified regulator for banking, capital markets, and insurance, among other areas, with the goal of making India's IFSCs, such as the GIFT IFSC

Horizontal Enforcer:

Agency

Core Domain

MeitY (Min. of Electronics & IT)

Data & Privacy: Governs the DPDP Act. This is the new universal law.

Recognised by RBI as an SRO for financial markets regulated by RBI (2025 recognition)

Regulator

FACE (Fintech Association for Consumer Empowerment)

Digital lending / consumer protection in fintech — ethical lending, collections standards

Recognised by RBI as an SRO for (certain) fintech/digital-lending activities (RBI recognition announced 2024)

Regulator

DLAI / Unified Fintech Forum (formerly DLAI)

Digital lending / fintech industry body — lender practices, advocacy

Industry association of digital lenders (DLAI has evolved; now referenced as Unified Fintech Forum)

Industry Body

General Insurance Council (GI Council)

General insurance industry representation, industry coordination

Representative body of general insurers (registered with IRDAI; statutory recognition under Insurance Act provisions)

Industry Body

Life Insurance Council

Life insurance industry coordination, industry data and policy dialogue

Statutory/industry council for life insurers (constituted under Insurance Act provisions)

Regulator

DPI:

The "Rail" (Protocol)

Primary Use

Enabling Body

Key Regulated Entities & Roles

UPI (Unified Payments Interface)

Move Value

NPCI (National Payments Corp.)

• PSPs (Payment Service Providers): The banks. • TPAPs (Third-Party App Providers): The FinTechs (e.g., GPay, PhonePe). • Payment Aggregators (PAs): Regulated by RBI.

AA (Account Aggregator)

Share Data

Sahamati (Industry Alliance / SRO)

• NBFC-AA: The only entity licensed by RBI to manage user consent. • FIP (Financial Info. Provider): The data source (e.g., Banks, Insurers). • FIU (Financial Info. User): The data consumer (e.g., Lenders, RIAs).

OCEN (Open Credit Enablement Net.)

Request Credit

(Protocol spec, often via iSPIRT)

• LSP (Loan Service Provider): The FinTech app (subject to DLG rules). • TSP (Technology Service Provider):E.g., an "LSP for LSPs." • Lenders (REs): The RBI-regulated NBFCs or Banks.

ONDC (Open Network for Digital Comm.)

Discover Commerce

DPIIT / ONDC (Section 8 Co.)

• Buyer-Side Apps: The consumer-facing app. • Seller-Side Apps: The merchant-side app. • (Regulation is indirect, via the network's rules and the underlying PA/LSP rules).

CBDC (Central Bank Digital Currency)

New Money

RBI

• Pilot Participants: Select banks authorized by RBI to distribute and manage e-Rupee wallets. • Interoperable with UPI.

Sign-up to my newsletter

I talk about start-up, investing, tech and everything around it. Sign-Up for my weekly newsletter to never miss an update